Buying notes and worried you’ll run out of funds for the next deal?

When note investors want to recapitalize, we often turn to note hypothecation or a partial structure. But what’s the difference and is one better than the other? Who wins in the matchup between hypothecation vs partials when buying mortgage notes?

What is Hypothecation?

Have you ever borrowed money against your home or car? Then you have used hypothecation.

Hypothecation happens when an asset is pledged as security for a loan without transfer of ownership.

It’s a fancy word for borrowing money against something you own.

It’s funny. Nobody says I just hypothecated my house. We say, we got a home loan or a mortgage.

When you get the loan, you retain possession and ownership of the home or car, while the lender has a lien they place against that collateral. If the money isn’t repaid timely the bank can enforce their rights to take the asset back.

But what about hypothecating real estate notes?

Note investors hold a note and mortgage where they receive payments. That receivable is an asset secured by real estate. They don’t own the real estate. They own a note. They then use that note as collateral to borrow money.

In essence, a note investor gets a new loan against an existing loan they own. They receive payments on the note they own, and they make payments on the note they owe.

Why Do Note Investors Use Hypothecation?

Note investors borrow funds for the same reason real estate investors use mortgages. They can control more assets and grow a portfolio using leverage.

Along with growth, they can also take advantage of interest rate spreads to create a type of arbitrage.

Let’s say you are earning an 11% yield (or IRR) on a note purchased at a discount. If you can borrow against that same note and are only paying 8%, then there is the potential to earn a 3% spread between the two.

A Note Hypothecation Example

Nate, the Note Investor, holds a note and mortgage against a property worth $150,000. Hope, the happy homeowner, is making payments on time to the licensed servicer and still owes:

- Unpaid Principal Balance UPB: $99,444.14

- Note Rate: 10%

- Monthly Payment: $877.57

- Remaining Term: 348 months

Nate had bought the note at a discount a year ago through his LLC. He paid $92,150.55 for the right to receive the balance of $100,000 back at that time. This provided him an anticipated yield or Internal Rate of Return (IRR) of 11%

Nate has received a year of payments (360 minus 12 = 348 months left) and would like to recapitalize to buy another real estate note. It’s a good note. Hope pays on time and he doesn’t want to sell it.

He was recently approached by Fran, one of his financial friends. She is a seasoned investor and has a self-directed IRA she’d like to put to work. Fran is happy to earn 8% in her IRA. They agree on a loan from her IRA to Nate with the following terms:

- Loan Amount: $92,000

- Loan Rate: 8%

- Monthly Payment: $877.57

- Term: 181 months

Fran’s IRA would receive $877.57 per month for the next 181 months and then the loan to her IRA would pay off. At that time, there would still be approximately $78,971.80 owed by Hope and Nate would go back to receiving the $877.57 per month for the remaining 167 months (348 minus 181 = 167).

An Alternative Structure

What if Nate wants to recapitalize but doesn’t want to wait 181 months to receive a monthly cash flow? Another possible loan structure could be:

- Loan Amount: $92,000

- Loan Rate: 8%

- Monthly Payment: $680.75

- Term: 348

With this structure, Fran’s IRA would receive $680.75 per month for the remaining term of 348 months while Nate would receive $196.82 per month during the same time.

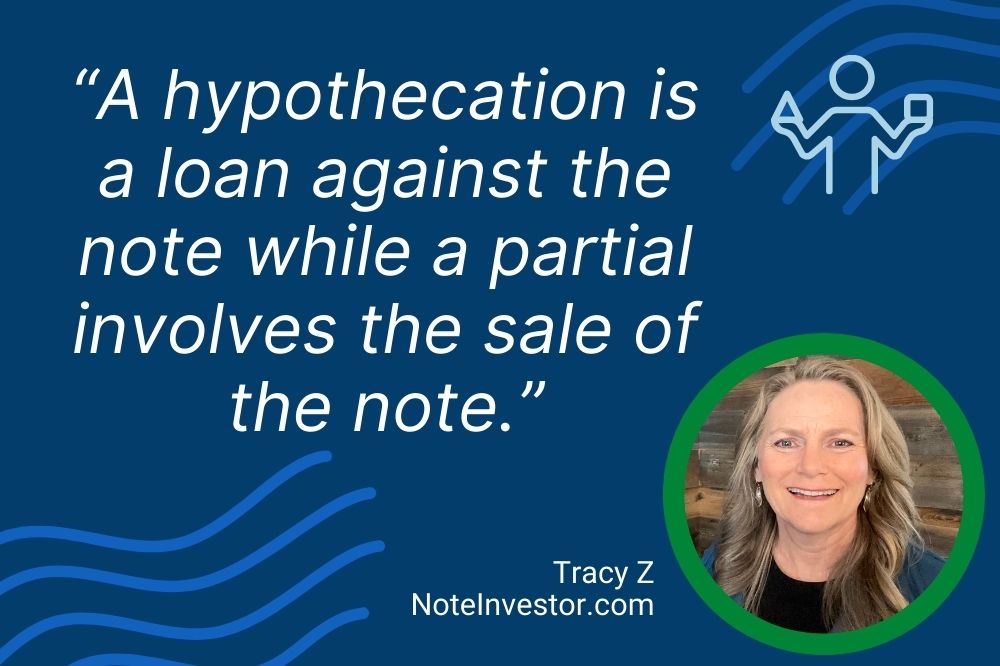

What’s the Difference Between Note Hypothecation and Partials?

A hypothecation is a loan against the note while a partial involves the sale of the note.

The biggest differences are the paperwork, the obligation, and who owns or controls the note.

When a real estate note is hypothecated, the holder of that notes continues to own and control the asset. They sign a new note and loan agreement with the lender. The lender then takes assignment of the existing note & mortgage asset for collateral purposes.

That differs from a note sale.

With the note sale, the note is fully transferred to a new investor using a full assignment and endorsement to the note.

That new investor becomes the note owner of record and holder in due course (HDIC). They control the asset for the time they receive payments. The primary recourse is against the property owner and the property itself.

There is also a purchase agreement. When the sale involves a partial, the agreement will additionally outline the terms of that partial arrangement. For more details read our article dedicated to What Is A Partial Note Purchase.

Documentation for Hypothecating Real Estate Notes

When hypothecating real estate notes, there are two sets of documentation. The first set of applies to the Existing Note and Mortgage against the property, and the second set applies to the loan against that asset.

Existing Note Documentation

This is an existing note and lien against the property that was signed by the property owner (as borrower) to the lender or seller financier (as mortgagee or beneficiary) when the borrower bought the property.

- Promissory Note – the property owner’s obligation to pay

- Mortgage or Deed of Trust – the lien against the real estate

There is also a full collateral file with the standard supporting due diligence documents.

Note Hypothecation Documentation

This second set of documentation is the loan extended to the note investor. It includes:

- Commercial Promissory Note – the note investor’s obligation to pay new lender

- Loan Agreement – between note investor and new lender

- Collateral Assignment of Existing Mortgage (or Deed of Trust)

- Note Endorsement to Existing Note – also referred to as an allonge

The new lender will also want to review the full collateral file on the existing note. They may also ask for underwriting documentation on the note investor obtaining the loan.

You’ll notice a purchase agreement is not used in a hypothecation. This differs from a note sale.

Differences to Note Sale Documentation

With a sale of the note there is the same set of existing note documentation, but the second set looks different:

- Full Assignment of Existing Mortgage (or Deed of Trust)

- Note Endorsement to Existing Note – usually endorsed “without recourse”

- Purchase & Sale Agreement (PSA) – also referred to as a Mortgage Purchase Agreement (MPA) or Receivable Purchase & Sale Agreement (RPSA)

You’ll notice with a note sale, they do not use a new commercial promissory note or loan agreement and the assignment/endorsement are full transfers rather than for collateral purposes.

As with all legal transactions, you’ll want to work with qualified legal counsel to determine what is best for your state.

What About Potential Tax Implications?

Since one is treated as a loan against an asset and the other is treated as the sale of an asset, the tax treatment varies.

If the note is owned by and held in a self-directed IRA, there can be advantages to using the partial approach to recapitalize. Since the partial is a sale of the asset, this avoids using debt financing within the IRA which can potentially incur Unrelated Business Income Tax (UBIT) through Unrelated Debt Financing Income (UDFI).

If the note is held outside of a tax advantaged retirement account, there can be benefits to using a hypothecation as the interest paid on the debt can have the ability to be used as an expense.

Of course, personal situations vary so use a qualified tax professional to determine what strategy is best for your individual circumstances and goals.

The Pros and Cons of Note Hypothecation

While both hypothecation and partial structures can provide capital to note investors for reinvestment, there are pros and cons when comparting the two.

Pros of Note Hypothecation

- Documentation can be easier to understand

- Potentially friendlier for private investors

- Terms of repayment can be negotiated

- Note Investor retains more control over the asset

- Options for collateral swap if note pays off early

- Easier to retain existing servicer

Cons of Hypothecation

- Lender may underwrite note investor as the borrower

- May carry additional legal obligation to may payments

- Lender may ask for a personal guarantee

- Most institutional-level note buyers prefer the partial structure for more control

- May require servicing transfer depending on new investor

Final Thoughts – Hypothecation vs. Note Partials

It’s important to work with legal counsel to ensure that you are using the right documents and structuring the transaction to comply with any Securities & Exchange (SEC) regulations.

These strategies work best for performing notes with regular monthly payments. Using a third-party servicing entity, licensed in the state where the property is located, will provide protection to the borrower, lender, and investor.

Over the last 35 years, we’ve used both partials and credit lines with note hypothecations. We tend to place partials with the institutional level note buyers. When dealing with private investors, the hypothecation can be easier to explain. Regardless the structure, you want a transaction that is setup to make your lender/investor whole and will provide protection for all parties.

When buying notes, the money to fund your next deal may come from your last deal!

Great information.

Glad you enjoyed Carlton!